Welcome to Quanzhou Weihang Machinery Co.,Ltd.

The global hydraulic cylinder industry is poised for steady expansion in 2026, propelled by industrial automation, infrastructure development, and technological innovation. Backed by authoritative market data and emerging industry trends, this outlook dissects the key dynamics shaping the sector’s trajectory in the coming year.

1. Market Scale and Growth Trajectory

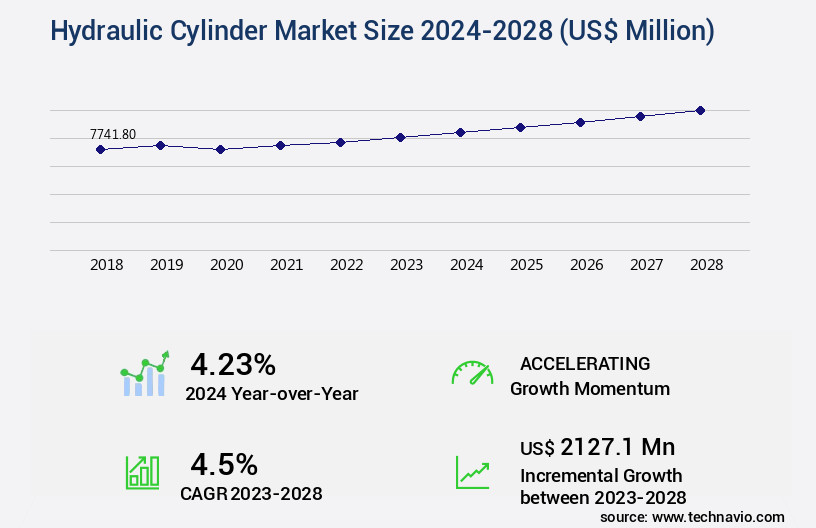

2026 marks a pivotal year for the hydraulic cylinder market, with dual growth engines in mature and emerging economies. Globally, the segment is expected to maintain a compound annual growth rate (CAGR) of 4.3% to 5.3%, building on its 2024 valuation of USD 12.4 billion for the broader fluid power cylinder market. Specifically, the hydraulic cylinder market alone is projected to reach USD 14.66 billion by 2026, driven by robust demand across end-use industries.

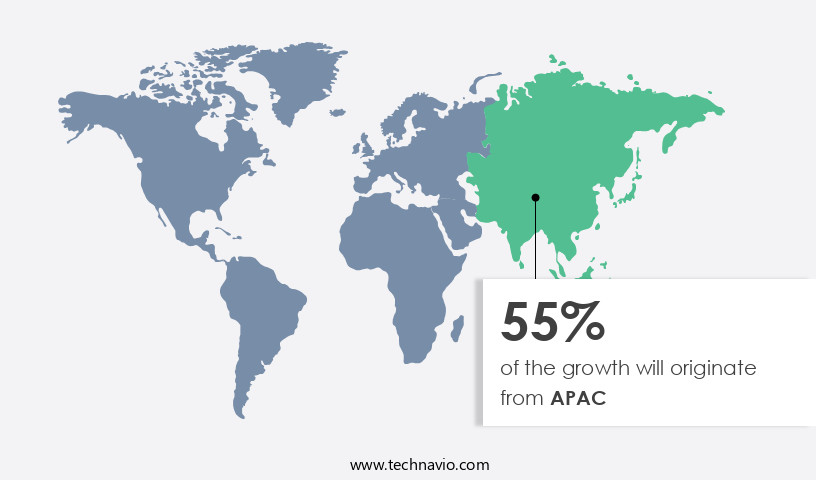

Regionally, China stands out as a high-growth market. After surpassing RMB 320 billion (approximately USD 44 billion) in 2025, China’s hydraulic cylinder sector is forecast to grow at a 6.8% CAGR in 2026, outpacing the global average. This acceleration stems from policy support for advanced manufacturing and infrastructure investment, with high-pressure cylinders accounting for over 58% of domestic production amid rising demand for heavy machinery. North America remains the largest regional market, while the Asia-Pacific region is emerging as the fastest-growing hub due to urbanization and industrialization drives.

2. Core Growth Drivers

2.1 Industrial Automation and Smart Manufacturing

The advancement of Industry 4.0 is reshaping demand for hydraulic cylinders. Manufacturers are increasingly integrating IoT sensors, digital twin technology, and remote monitoring capabilities into hydraulic systems, transforming traditional components into "intelligent terminals". In 2026, smart hydraulic cylinders—equipped for real-time performance tracking and predictive maintenance—are expected to capture over 25% of the high-end equipment market, particularly in automotive assembly and aerospace manufacturing. This shift enhances precision, reduces downtime, and aligns with global smart factory initiatives.

2.2 Infrastructure and Heavy Machinery Demand

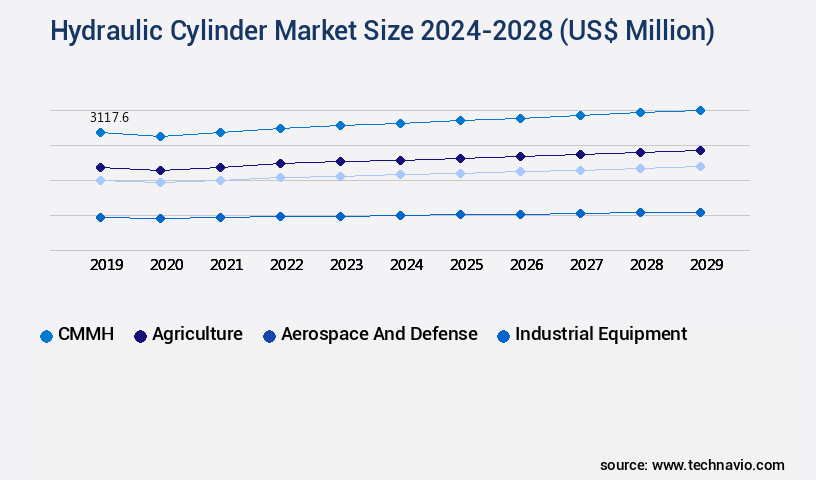

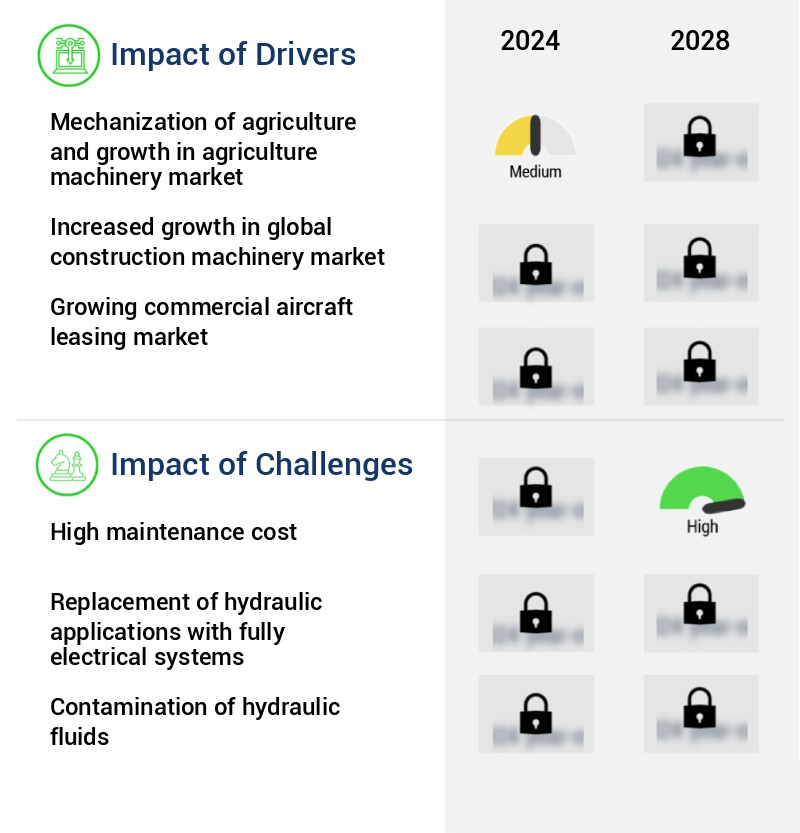

Global infrastructure development is a critical demand catalyst. In Asia-Pacific, projects like China’s "New Infrastructure" plan and Southeast Asian urban rail networks are boosting orders for hydraulic cylinders used in excavators, shield machines, and cranes. The Middle East’s ongoing construction boom, coupled with North America’s infrastructure renewal efforts, further fuels demand for heavy-duty hydraulic systems. Meanwhile, the mechanization of agriculture in India and Brazil is driving uptake in compact hydraulic cylinders for tractors and harvesters, expanding the sector’s application scope.

2.3 Sustainability and Regulatory Pressures

Stricter environmental regulations and the global "dual carbon" agenda are pushing the industry toward eco-friendly innovation. In 2026, manufacturers will prioritize energy-efficient designs, such as electro-hydraulic hybrid systems that bridge traditional hydraulics with digital controls to compete with electric actuators. Green manufacturing processes—including acid-free surface treatment and energy-saving forging—are becoming mandatory for compliance, particularly in the European Union and China. These measures not only reduce carbon footprints but also improve operational efficiency, with energy-saving hydraulic systems delivering up to 15% lower power consumption compared to conventional models.

3. Technological Innovation and Product Evolution

3.1 Lightweight and High-Performance Materials

Material science breakthroughs are redefining product capabilities. To address weight reduction demands in mobile equipment, manufacturers are adopting high-strength aluminum alloys and composite materials for non-pressure-bearing components, reducing overall cylinder weight by 20–30% without compromising durability. For high-pressure applications, domestically produced specialty steels (led by Chinese giants like Baowu and Citic Special Steel) are replacing imports, accelerating localization and cost control. Advanced sealing technologies, resistant to extreme temperatures and corrosion, are extending product lifespans by 40% in harsh mining and oil & gas environments.

3.2 Integration of Digital and Hydraulic Technologies

Electro-hydraulic servo systems are becoming mainstream in 2026, offering superior control precision for semiconductor manufacturing and aerospace applications. These systems integrate seamlessly with industrial IoT platforms, enabling centralized monitoring of multiple cylinders in real-time. For example, in wind turbines, smart hydraulic cylinders for pitch control now feature self-diagnostic functions that reduce maintenance costs by 25% annually. Digital twin technology is also gaining traction, allowing manufacturers to simulate cylinder performance under varying loads and optimize designs before production.

4. Regional Market Dynamics

4.1 China: From Scale to Quality

China’s market is undergoing a structural shift from low-cost mass production to high-value manufacturing. Leading enterprises like Hengli Hydraulic and Eddy Precision control 18.5% and 12% of the domestic market, respectively, focusing on high-pressure, long-stroke cylinders for new energy and aerospace sectors. Export growth is another key driver, with shipments to "Belt and Road" countries rising by 12.1% annually, led by excavator and agricultural machinery cylinders. However, the market remains fragmented among small and medium-sized enterprises (SMEs) in the low-end segment, where profit margins are squeezed by raw material price volatility.

4.2 North America and Europe: Technological Leadership

North America leads in smart hydraulic cylinder adoption, driven by the aerospace & defense and material handling industries. European manufacturers, such as Bosch Rexroth and Bucher Hydraulics, are pioneering energy-efficient designs to meet the EU’s strict emissions standards. Both regions are witnessing a surge in demand for custom-engineered cylinders for automated warehouses, spurred by the growth of e-commerce and logistics automation.

4.3 Emerging Markets: Untapped Potential

Southeast Asia, the Middle East, and Africa are emerging as high-growth regions in 2026. Infrastructure investments in Vietnam and Indonesia, coupled with mining activities in South Africa, are driving demand for mid-range hydraulic cylinders. Local manufacturers are partnering with global players to access technology, while international firms are establishing production hubs to avoid import tariffs and shorten delivery times.

5. Challenges and Mitigation Strategies

5.1 Raw Material Volatility

Specialty steel and high-performance seals account for 60% of production costs, and price fluctuations (such as the 2022 steel price surge) have strained SME profitability. To mitigate risks, leading companies are signing long-term supply contracts and investing in vertical integration—for instance, Hengli Hydraulic has established in-house seal production to reduce dependency on imports.

5.2 Competition from Electric Actuators

Electric cylinders are gaining market share in light-duty applications due to their lower noise and higher energy efficiency. In response, hydraulic manufacturers are developing hybrid electro-hydraulic systems that combine the high force of hydraulics with the precision of electric controls. These systems are particularly competitive in medium-load scenarios, such as food processing and packaging, where both power and accuracy are required.

5.3 Supply Chain Resilience

Global supply chain disruptions, exacerbated by geopolitical tensions, have highlighted the need for localization. In China, the "Industrial Strong Foundation Engineering" policy supports domestic production of key components, while European firms are shifting suppliers from Asia to Eastern Europe. Digital supply chain management, including real-time inventory tracking, is also helping companies anticipate shortages and adjust production schedules.

6. Conclusion

2026 will be a year of transition for the hydraulic cylinder industry, characterized by steady growth, technological upgrading, and market polarization. The global market will expand at a 4.3–5.3% CAGR, with China leading regional growth at 6.8%. Key trends—smart manufacturing integration, sustainability, and material innovation—will define competitive advantage, while challenges like raw material costs and electric actuator competition will drive industry consolidation.

For stakeholders, opportunities lie in high-end product development (e.g., smart hydraulic systems for wind energy), emerging market penetration, and green manufacturing. Companies that prioritize R&D, supply chain resilience, and customer-centric customization will thrive in this evolving landscape, while those reliant on low-cost, low-tech production may face marginalization. As the industry adapts to automation and sustainability demands, hydraulic cylinders will remain indispensable in heavy-industry applications, proving their enduring value alongside advancing technologies.

Quanzhou Weihang Machinery Co.,Ltd.